When you’re thinking about taking out a personal loan, the interest rate can feel confusing, adding to the pressure of making the right choice. You’re trying to deal with an urgent expense, your credit might not be in the best shape, and now you’re staring at numbers, wondering how interest works on a personal loan, and what this means for your budget.

What does interest mean on a personal loan?

Interest is the cost you pay to borrow money. When a lender gives you a personal loan, they charge interest as a percentage of the amount you borrow, and that charge is spread across your monthly installment loan payments.

It’s also important to know that the interest rate you see advertised isn’t always the rate you’ll receive. Advertised rates are usually representative, meaning they’re based on borrowers with stronger credit profiles. The rate you’re actually offered is set after the lender reviews your application and looks at your income, credit history, existing debts, and loan term. This is why two people can apply for the same loan and receive very different rates, as the final interest rate reflects individual circumstances, not just the headline figure.

How does the interest rate work on a personal loan?

Most personal loans use a fixed rate of interest, which means your rate remains the same from start to finish, as agreed in the initial loan offer. Your monthly payments won’t change, and you’ll know exactly what the loan will cost over time.

Lenders set your rate by looking at your credit, income, and your debt-to-income ratio. If your credit is low or your budget is already stretched, the rate might be higher compared to someone with stronger credit because lenders see more risk in the loan.

Rates also vary based on how much you borrow and how long you plan to repay the loan. A short-term loan will come with a lower rate of interest but a higher monthly payment, while longer terms will have higher rates of interest but smaller monthly payments.

Even small changes in a rate can affect what you pay overall. For example, a few percentage points can add hundreds of dollars to the total cost, depending on the loan size and repayment length. Getting your head around this helps you judge if an offer fits your budget.

While your own finances decide the rate you’re offered, wider interest rates matter too. The Federal Reserve sets a base rate that affects how much it costs lenders to borrow money. When that rate goes up or down, personal loan rates often shift the same way, even though your final rate is still based on your situation.

How Interest Is Calculated on a Personal Loan

Most personal loans use simple interest, which makes it easier to see how much you’ll pay in interest over time. Simple interest is based on your loan amount, your loan interest rate, and your loan term.

Each monthly payment includes a portion that goes toward interest and a portion that reduces the principal (the amount you borrowed). Early in the schedule, more of the payment goes toward interest, and that balance shifts as the principal gets smaller.

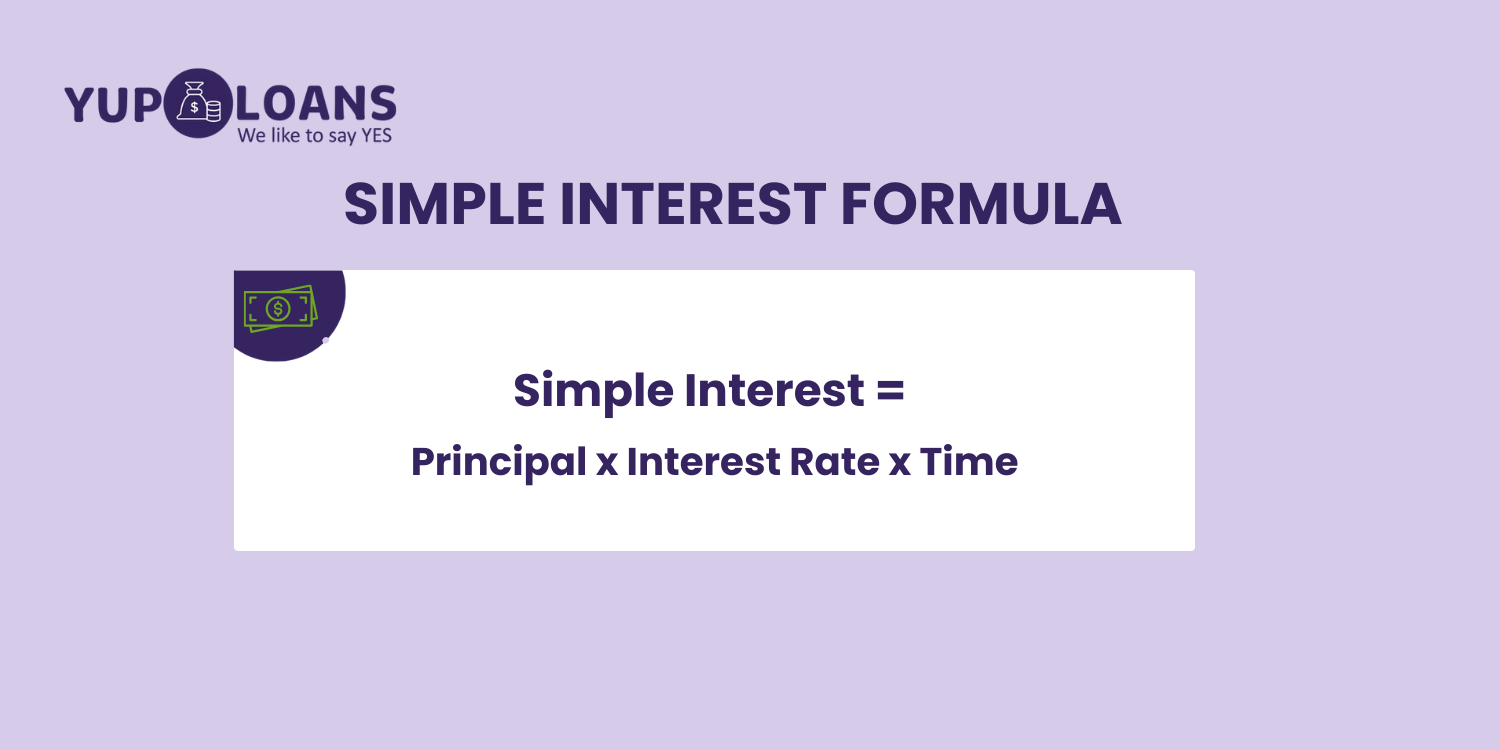

A simple way to see how interest works is with this formula:

Simple Interest = Principal × Interest Rate × Time

A Simple Interest Worked Example

If you borrow $2,000 at a 12% personal loan interest rate for one year, using simple interest:

$2,000 × 0.12 × 1 = $240 in total interest

That $240 is spread across your monthly payments, along with part of the principal. If you choose a longer loan term, your monthly payment drops, but your total interest increases because the interest accrues over a longer period. A shorter loan term has higher payments but lower total interest, which is why the length of the loan can affect the interest as much as the rate itself.

Annual Percentage Rate (APR) vs Interest Rate: Why the Difference Matters

When you compare loan offers, it helps to understand the difference between the loan interest rate and the annual percentage rate.

The interest rate is the cost of borrowing the principal, but APR goes a step further by including lender fees, so it gives you a clearer view of the interest costs you’ll pay over the life of the loan.

Because most unsecured personal loans use simple interest (rather than compound interest), the interest rate itself is straightforward. But fees can still change the amount of interest you pay overall. This is why two loans with the same interest rate can have different APRs, and why APR often offers a better comparison point when you’re looking at the best personal loan rates.

What affects the loan interest rate you’re offered?

When you apply for a personal loan, lenders look at several pieces of your financial picture to decide your personal loan interest rate. Your credit history is one part of it, but it’s not the only thing that influences the offer you receive.

Your income and monthly expenses matter because they show how comfortably you can repay a loan. If most of your paycheck is already tied up in bills (a high credit utilization ratio), or you’re carrying balances on credit cards or student loans, the lender might see a higher risk and adjust the interest rate accordingly.

The loan amount and loan term will also have an impact, as borrowing more or stretching the loan out longer can increase the interest charged, since the lender is taking on risk over a longer period.

Some lenders, including many in the Yup Loans network, also pay attention to things like steady deposits, time with your bank, or alternative income sources. These details can help when your credit isn’t perfect and lead to a more favorable interest rate than you expect. Because every lender weighs these factors differently, comparing loan offers is one of the best ways to find terms that fit your budget.

Ways to Lower the Personal Loan Interest Rate You’re Offered

Borrow Only What You Need

A smaller loan amount often results in lower interest rates because interest accrues on a smaller balance. Keeping the request realistic also helps when you’re trying to secure the loan with a favorable interest rate.

Choose a Shorter Loan Term When You Can

A shorter loan term usually means higher monthly payments but lower total interest across the life of the loan. Since your interest is typically based on how long you borrow, reducing the time can make a noticeable difference.

Work on Your Credit Before Taking Out a Loan

Paying down balances, correcting errors, and avoiding late payments can improve your chances of receiving a lower interest rate. This can help when lenders review your financial profile and set the personal loan interest rate on your application.

Consider a Cosigner if the Lender Allows It

A cosigner with stronger credit can help you secure the loan at a better rate. Lenders might feel more confident in the shared responsibility and give a lower interest rate.

Compare Loan Types & How Interest Is Calculated

Not every type of personal loan works the same way. Many personal loans use simple interest, which is easier to manage. Others use precomputed interest, which can limit how much you save if you pay the loan off early. Loans or credit products that use compound interest tend to cost more because the balance grows faster. Reviewing these differences helps you save on interest and choose the best fit.

How Extra Monthly Payments Can Affect the Interest

If your lender allows it, paying a little more than the scheduled monthly payment can shorten the loan term and reduce the total interest without requiring a full refinance. This works because interest accrues daily on many loans, so lowering the balance even mid-month can make a difference in how much you’ll pay in interest over time. Borrowers who want to pay the loan off early often benefit from this approach, especially if they can avoid prepayment penalties.

Extra loan payments don’t have to be large to help. Tucking away tax refunds, bonuses, or any unexpected income and putting it toward your loan can reduce interest expenses more effectively than spreading that money across smaller bills. Over time, these small steps can bring the balance down faster and help you reach a lower total interest cost.

Find a Personal Loan With Clear Interest Terms

When you need to get your finances sorted quickly, shopping around for the best interest rates can feel overwhelming. Yup Loans simplifies that process. With one quick loan application, we connect you with a lender from our network that best fits your situation. You’ll receive a single loan offer with clear details, including the loan interest rate, the loan term, the loan amount, and the annual percentage rate, so you know exactly what the loan will cost over the life of the loan.

Yup Loans gives you an easy way to compare your real costs, understand the interest charged, and choose whether to move forward. Request funds today to get started.